global perspectives

Simply put: where are rates headed?

This article marks the first of a regular series chronicling our multi-asset team’s perspectives.

In a nutshell, we currently believe:

• The improvement in GDP growth could spur a partial normalisation in savings and a tapering phase by central banks

• Both elements could lead to roughly a 50bps rise in real rates in the US, in our opinion

• This is sufficient to spur negative performance in bonds by year-end, but small enough that it remains limited in total returns terms

With the Federal Reserve’s Jackson Hole meeting now past, it’s a good juncture to reflect on the level of rates in the medium term. Rates are low – that is a statement – and the temptation to see them mean-reverting to higher levels is common. We ask the essential questions: what factors explain the low level of rates, and what is their likely behaviour in the medium term?

Based on the work of Irving Fisher1, general academia sees three components comprising each tenor of the yield curve:

- the inflation premium: how much inflation compensation the market agrees on for holding bonds

- a term structure premium: how much compensation the market requires to offset duration risk

- what remains: “real rates”, what the buy-and-hold investor will retain at the maturity of the bond in real terms – that is to say net of inflation impact

The term structure impact is usually small. We believe the current inflation shock is likelier to be transient than persistent, meaning inflation compensation should remain low. Should inflation mean-revert to where it was prior to the pandemic, markets are unlikely to seek much more protection than what they already have, in our opinion.

The drivers of real rates

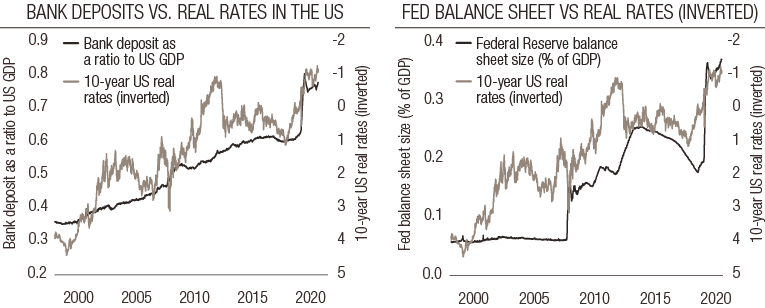

Focusing on real rates, figure 1 highlights two key drivers of real rates: savings and monetary policy.

First, economic theory clearly states that real rates bring balance between capital owners (households and corporates savings) and those in need of it (investors). A high level of savings in a context of low investment means naturally lower real rates. Today, consumer survey data2 clearly shows pessimism, while investment intent surveys3 lay on the lower end of their historical evolution. This means that the level of accumulated savings will keep bearing lower on real rates for probably longer than expected.

The level of savings is approximated by looking at US bank deposits as a ratio of GDP, and are illustrated in figure 1: some USD 2 trillion remains in excess of the pre-pandemic period. These savings will normalise as macro conditions do, but the process stands a good chance of lasting a long time.

Second, current accommodative monetary policy explains the remainder: as central banks have purchased bonds they have compressed real rates, pushing investors to exit the bond market to buy equities – also known as the “risk appetite” monetary policy channel.

Figure 1. US bank deposits vs real rates and the Fed’s balance sheet vs rates

Source : Bloomberg, LOIM. For illustrative purposes only.

Figure 1 shows a clear illustration of this phenomenon. The Jackson Hole meeting was slightly more dovish than expected, but also set out the Fed’s medium term goal: exiting its current accommodative stance. There is no precise calendar for that, but current expectations are for the Fed’s balance sheet to fully stabilise by the end of 2022/beginning of 2023. From the figure, a stabilisation of the Fed’s balance sheet in GDP terms is not enough to see real rates rise. For that, we need to see the world economy’s growth rate outpace the growth rate of central banks’ holdings.

One common denominator of both factors is therefore GDP growth: should it surprise to the upside in coming quarters, then real rates stand a chance of rising. This would create confidence for consumers and corporates, pushing them to reduce their savings (for consumption and investment). It would reduce the Fed’s balance sheet size relative to GDP, pushing rates higher. In the 1930s and after World War II, a similar process was instrumental to exiting a period of sharply negative real rates.

How high could rates go?

The final question is: if rates increase as real-rates factors improve, how high can they go? Let’s do the maths. If savings normalise fully (which is unrealistic) and bank deposits move back to 60% of the US GDP (their pre-pandemic level, from roughly 75% now), a historical regression would restore real rates to a positive 1%. This would bring nominal rates to about 3%, which means a price return of about -15%.

We believe this is an unrealistic scenario for the following reasons:

- the carry on bonds is positive and would increase as rates rise

- the beginning of quantitative easing was orderly across the world – the exit will not be the same

- in 2008, risk aversion savings normalised by roughly 25%; in the current scenario that would mean a 50bps increase in real rates

With that 2008 scenario in mind, we believe it is reasonable to expect the US 10-year nominal rate to reach 1.8% by year-end – perhaps with some volatility. Accounting for carry, a-synchronicity and normalising inflation, we do not expect major losses on our bond investments4. Quite the contrary, with continued pandemic uncertainty, we remain happy with bonds’ diversification potential.

Medium-term outlook

Simply put: rates could rise as real rates increase in the quarters to come. Yet we believe this rise should be limited, as savings and monetary policy are in the driving seat and unlikely to dramatically normalise.

Quellen

Wichtige Informationen.

NUR FÜR PROFESSIONELLE INVESTOREN

Dieses Dokument wurde von Lombard Odier Funds (Europe) S.A. herausgegeben, einer in Luxemburg ansässigen Aktiengesellschaft mit Sitz an der Route d’Arlon 291 in 1150 Luxemburg, die von der Luxemburger Finanzmarktaufsichtsbehörde, („CSSF“), als Verwaltungsgesellschaft im Sinne der EU-Richtlinie 2009/65/EG in der jeweils geltenden Fassung und der EU-Richtlinie 2011/61/EU über die Verwalter alternativer Investmentfonds (AIFMD-Richtlinie) zugelassen wurde und deren Aufsicht unterstellt ist. Geschäftszweck der Verwaltungsgesellschaft ist die Errichtung, Vermarktung, Administration, Verwaltung und der Vertrieb von luxemburgischen und ausländischen OGAW, alternativen Investmentfonds („AIF“) sowie anderen regulierten Fonds, kollektiven und sonstigen Anlagevehikeln sowie das Angebot von Portfolioverwaltungs- und Anlageberatungsdiensten.

Lombard Odier Investment Managers („LOIM“) ist ein Markenzeichen.

Dieses Dokument wird ausschließlich zu Informationszwecken bereitgestellt und stellt weder ein Angebot noch eine Empfehlung zum Kauf oder Verkauf eines Wertpapiers oder einer Dienstleistung dar. Es darf nicht in Rechtsordnungen verbreitet, veröffentlicht oder genutzt werden, in denen eine solche Verbreitung, Veröffentlichung oder Nutzung rechtswidrig wäre. Dieses Dokument enthält keine personalisierte Empfehlung oder Beratung und ersetzt keinesfalls eine professionelle Beratung zu Anlagen in Finanzprodukten. Anleger sollten vor Abschluss eines Geschäfts die Angemessenheit der Investition unter Berücksichtigung ihrer persönlichen Umstände sorgfältig prüfen und gegebenenfalls einen unabhängigen Fachberater hinsichtlich der Risiken und etwaiger rechtlicher, regulatorischer, finanzieller, steuerlicher und buchhalterischer Auswirkungen konsultieren. Dieses Dokument ist Eigentum von LOIM und wird den Empfängern ausschließlich zum persönlichen Gebrauch überlassen. Es darf ohne vorherige schriftliche Genehmigung von LOIM weder ganz noch auszugsweise vervielfältigt, übermittelt, abgeändert oder für einen anderen Zweck verwendet werden. Dieses Dokument gibt die Meinungen von LOIM zum Datum seiner Veröffentlichung wieder.

Weder das vorliegende Dokument noch Kopien davon dürfen in die USA, in die Gebiete unter der Hoheitsgewalt der USA oder in die der Rechtsprechung der USA unterstehenden Gebiete versandt, dorthin mitgenommen, dort verteilt oder an US-Personen bzw. zu deren Gunsten abgegeben werden. Als US-Person gelten zu diesem Zweck alle Personen, die US-Bürger oder Staatsangehörige sind oder ihren Wohnsitz in den USA haben, alle Personengesellschaften, die in einem Bundesstaat oder Gebiet unter der Hoheitsgewalt der USA organisiert sind oder bestehen, alle Kapitalgesellschaften, die nach US-amerikanischem Recht oder dem Recht eines Bundesstaates oder Gebiets, das unter der Hoheitsgewalt der USA steht, organisiert sind, sowie alle in den USA ertragssteuerpflichtigen Vermögensmassen oder Trusts, ungeachtet des Ursprungs ihrer Erträge.

Datenquelle: Sofern nicht anders angegeben, wurden die Daten von LOIM aufbereitet.

Obwohl gewisse Informationen aus als verlässlich geltenden öffentlichen Quellen stammen, können wir ohne eine unabhängige Prüfung die Genauigkeit oder Vollständigkeit aller aus öffentlichen Quellen stammenden Informationen nicht garantieren.

Die in diesem Dokument geäußerten Ansichten und Einschätzungen dienen ausschließlich Informationszwecken und stellen keine Empfehlung von LOIM zum Kauf, Verkauf oder Halten von Wertpapieren dar. Die Ansichten und Einschätzungen entsprechen dem Stand zum Zeitpunkt dieses Dokuments und können sich ändern. Sie sind nicht als Anlageberatung zu verstehen.

Dieses Material darf ohne vorherige Genehmigung von Lombard Odier Funds (Europe) S.A. weder vollständig noch auszugsweise (i) in irgendeiner Form oder mit irgendwelchen Mitteln kopiert, fotokopiert oder vervielfältigt oder (ii) an Personen abgegeben werden, die nicht Mitarbeiter, leitende Angestellte, Verwaltungsratsmitglieder oder bevollmächtigte Vertreter des Empfängers sind. ©2021 Lombard Odier IM. Alle Rechte vorbehalten.