global perspectives

Simply put: energy inflation is transitory, unlike shelter costs

In our latest multi-asset macro update, we share the following views:

- The recent US inflation report highlights several key contributors to rising inflation, not just energy.

- The cost of shelter has risen and is likely to continue to drive inflation over the medium term, reflecting the rapid rise in house prices and the lagging impact this can have on inflation measures.

- Both the Federal Reserve and investors will need to pay close attention to this factor in the months ahead.

Markets and central banks have been discussing the supposedly ‘transitory’ nature of inflation. The factors being heavily scrutinised include energy prices, supply-chain bottlenecks and labour-supply shortages (notably in the US). Most of these factors have impacts that are lagging and vary in size and duration, which combine into a temporary elevation of inflation that is pushing central bankers out of their comfort zone.

The latest US monthly inflation report is no exception and once more confirms the importance of the inflation theme to market activity. We think the key takeaway from this report is that energy inflation is less likely to surprise on the upside than ‘service’ inflation – an inflation source that is slow to take effect yet is strongly tied to the good economic conditions we are experiencing today.

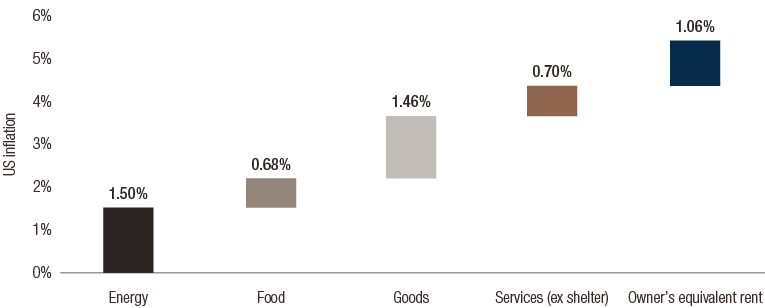

US headline inflation reached 5.4% in September and its core reading rose to 4%. In our view, there are three factors behind this:

- Energy continues to be the largest contributor to inflation, adding 1.5% year-on-year. This shouldn’t be surprising given oil prices have risen by around 100% year-on-year. Such base effects have material consequences on inflation numbers, but oil prices would need to reach $160 per barrel over the next 12 months to maintain this high level of contribution.

- Food and goods inflation added around 2% to inflation. Over the longer run, food inflation should evolve around 2% while goods inflation will be roughly zero, meaning this should also be a source of temporary headline inflation.

- The final element – service inflation – is our key focus here. This has contributed roughly 1.7% to inflation, two thirds of which has been the outcome of an element which is technically not even a service: the cost of shelter. The cost of shelter has risen 3.2% year-on-year and represents a 30% weight in the inflation basket.

FIG. 1. Year-on-year US Inflation Decomposition

Source: Bloomberg, LOIM at October 2021. For illustrative purposes only.

Within the “shelter” component, one particular element has a sizeable weight on its own: the owner’s equivalent rent of primary residence (OER). The OER’s weight in the headline CPI is 23.6%, accounts for 29.9% in the core CPI, and in the personal consumption expenditure (PCE) basket, its weight stands at 11.4% for headline and 12.9% for core. The OER therefore considerably affects the evolution of prices and monetary policy. In our eyes, this component needs to be monitored closely to anticipate the evolution of inflation.

In order to understand how this number might evolve, understanding how it is calculated is crucial. The Bureau of Labor Statistics (BLS) measures the OER using a survey, where primary residence owners are asked how much rent they think they would be charged if they were to rent their home instead of owning it. This component is therefore derived from the perceived value of property owners’ homes and multiple factors can affect it.

Research from the Federal Reserve (Fed) Bank of Cleveland finds that the strongest driver of OER inflation is lagged house-price appreciation – if owners perceive their house prices have risen, then their answer to the survey is likely to increase. So what are house prices doing right now? The US Case-Shiller index is currently showing a 20% year-on-year increase in house prices, a growth rate that has not been seen during the 1988-2021 period. As illustrated in figure 2, the historical relationship between house prices and OER increases highlights two key elements:

- Firstly, their relationship tends to lag by 18-months – it takes a long time for OER inflation to materialise and then remains on a rising trajectory for a long time.

- Secondly, having already seen a significant rise in house prices, a linear regression forecasts the OER to grow at a 4.5% rate in 18 months’ time.

This projection should yield an inflation contribution of 1.3% to core inflation during the medium term and 0.5% to the PCE aggregates.

FIG. 2. OER year-on-year inflation versus house prices relative variations

Source: Bloomberg at October 2021. For illustrative purposes only.

Two additional variables that could also directly or indirectly influence OER are financial conditions and wages. Financial conditions are driven by return expectations from an asset-owner’s perspective, while wages tend to represent a measure of affordability. In the current environment, both of these factors could further fuel OER as being an essential source of durable inflation in the US.

If the Fed wants to meet its medium-term inflation goal, it should regard these prospects with a friendly eye. However, rapidly rising housing prices could well create an upside inflation risk that requires a more rapid monetary policy adjustment than initially expected. In our view, this is where the inflation risk lies today, not with commodities.

|

Simply put, inflation should remain elevated for some time – not because of the increasing price of commodities, but due to rising shelter costs. We believe this factor could affect longer term rates and Fed policy, and will require close scrutiny by investors. |

informations importantes.

À l’usage des investisseurs professionnels uniquement

Le présent document a été publié par Lombard Odier Funds (Europe) S.A., société anonyme (SA) de droit luxembourgeois, ayant son siège social sis 291, route d’Arlon, 1150 Luxembourg, agréée et réglementée par la CSSF en tant que Société de gestion au sens de la directive 2009/65/CE, telle que modifiée, et au sens de la directive 2011/61/UE sur les gestionnaires de fonds d’investissement alternatifs (directive GFIA). La Société de gestion a pour objet la création, la promotion, l’administration, la gestion et la commercialisation d’OPCVM luxembourgeois et étrangers, de fonds d’investissement alternatifs (« FIA ») et d’autres fonds réglementés, d’organismes de placement collectif ou d’autres véhicules d’investissement, ainsi que l’offre de services de gestion de portefeuille et de conseil en investissement.

Lombard Odier Investment Managers (« LOIM ») est un nom commercial.

Ce document est fourni à titre d’information uniquement et ne constitue pas une offre ou une recommandation d’acquérir ou de vendre un titre ou un service quelconque. Il n’est pas destiné à être distribué, publié ou utilisé dans une quelconque juridiction où une telle distribution, publication ou utilisation serait illégale. Ce document ne contient pas de recommandations ou de conseils personnalisés et n’est pas destiné à remplacer un quelconque conseil professionnel sur l’investissement dans des produits financiers. Avant de conclure une transaction, l’investisseur doit examiner avec soin si celle-ci est adaptée à sa situation personnelle et, si besoin, obtenir des conseils professionnels indépendants au sujet des risques, ainsi que des conséquences juridiques, réglementaires, financières, fiscales ou comptables. Ce document est la propriété de LOIM et est adressé à son destinataire pour son usage personnel exclusivement. Il ne peut être reproduit (en totalité ou en partie), transmis, modifié ou utilisé dans un autre but sans l’accord écrit préalable de LOIM. Ce document contient les opinions de LOIM, à la date de publication.

Ni ce document ni aucune copie de ce dernier ne peuvent être envoyés, emmenés ou distribués aux États-Unis, dans l’un de leurs territoires, possessions ou zones soumises à leur juridiction, ni à une personne américaine ou dans l’intérêt d’une telle personne. À cet effet, l’expression « Personne américaine » désigne tout citoyen, ressortissant ou résident des États-Unis d’Amérique, toute association organisée ou existant dans tout État, territoire ou possession des États-Unis d’Amérique, toute société organisée en vertu des lois des États-Unis ou d’un État, d’un territoire ou d’une possession des États-Unis, ou toute succession ou trust soumis dont le revenu est imposable aux États-Unis, qu’en soit l’origine.

Source des chiffres : sauf mention contraire, les chiffres sont fournis par LOIM.

Bien que certaines informations aient été obtenues auprès de sources publiques réputées fiables, sans vérification indépendante, nous ne pouvons garantir leur exactitude ni l’exhaustivité de toutes les informations disponibles auprès de sources publiques.

Les avis et opinions sont exprimés à titre indicatif uniquement et ne constituent pas une recommandation de LOIM pour l’achat, la vente ou la détention de quelque titre que ce soit. Les avis et opinions sont donnés en date de cette présentation et sont susceptibles de changer. Ils ne devraient pas être interprétés comme des conseils en investissement.

Aucune partie de ce document ne saurait être (i) copiée, photocopiée ou reproduite sous quelque forme et par quelque moyen que ce soit, ou (ii) distribuée à toute personne autre qu’un employé, cadre, administrateur ou agent autorisé du destinataire sans l’accord préalable de Lombard Odier Funds (Europe) S.A. Au Luxembourg, ce document est utilisé à des fins marketing et a été approuvé par Lombard Odier Funds (Europe) S.A., qui est autorisée et réglementée par la CSSF.

© 2021 Lombard Odier IM. Tous droits réservés.