investment viewpoints

Five reasons why the oil shock and COVID-19 may be positive for climate investment

Head of Sustainability Research

In the global COVID-19 pandemic countries are working to strike a balance between protecting health, preventing economic and social disruption, and respecting human rights. The pandemic is first and foremost a humanitarian tragedy but is now severely impacting on the global economy and has become intertwined with an oil price collapse and market turbulence across asset classes.

Historically, low oil prices would typically have a negative effect on the speed and scale of the transition to a net-zero economy. But today, market dynamics are much more complex. While some industries are likely to continue to suffer profoundly from the combined impact of the oil price crash and the COVID-19 virus, overall we expect this will have a positive impact for climate transition strategies. Changes in the policy environment, in consumer buying patterns and in the economics of renewable energy and clean transportation suggest the current oil price is actually a window through which one can glance at the future, rather than an impediment to the climate transition.

Sectors including legacy, fossil fuel energy and air travel are likely to see a prolonged negative effect. The lower oil price might initially be assumed to push back the event horizon for the clean mobility transition, and prospects for electrification more generally, but the positive feedback loop of policy, market forces and consumer dynamics look increasingly supportive for the ongoing decarbonisation of the sector. Renewables, all sorts of green technologies (e.g. biomaterials, precision farming, alternative proteins, clean/lean manufacturing) and their enabling infrastructure (e.g. transmission/distribution, storage and digital systems) as well as the emergent hydrogen economy are all well positioned for continued growth. The clean, lean and circular revolution underway in industry is based quite simply on a fundamentally better economic proposition than that of legacy industry, and will not be hampered by the market turbulence we are seeing today.

There are five key reasons why we believe the oil price shock may well accelerate the transition to a net-zero economy:

Policy has reached critical momentum to drive the transition forward despite the dramatic change in the oil price. Take mobility, for example. A growing number of cities are banning internal combustion engines and regulations limiting fleet-level carbon emissions mean car manufacturers are under increasing pressure to incentivise consumers to buy electric vehicles (EVs) to avoid heavy fines. These policy effects work to counteract the fall in the oil price.

Policy supporting the deployment of clean energy and transportation draws its impetus in many regions, including China, not only from climate change, but increasingly also from the profound human health and economic costs of severe local air pollution. The World Health Organization (WHO) estimates that air pollution kills more people than smoking every year globally (about 9 million people a year globally), and coal-fired power generation as well as diesel and gasoline vehicles are largely to blame.

Health considerations combine with radically improved cost points (see below) for all types of clean energy and mobility. Green technology levalised costs have fallen by up to 80% compared to the cost points of 2008/09 during the last major rounds of fiscal stimulus, when green infrastructure was a key beneficiary. We therefore expect to see a rapid escalation in low-carbon, growth-boosting fiscal stimulus as governments globally fight to counteract the recessionary impact of the COVID-19 virus.

The EU has already announced its USD 1 trillion Green Deal, which is designed to get the bloc to net-zero by 2050 - a trajectory that is likely to be enshrined into law in the near future. Green investments are also a key focus of China’s stimulus package announced in June 2019. In the US, new polling has found that there is broad support for massive investment in green technology1.

Central banks are also increasing the pressure behind the climate transition. The Bank of England, for example, announced a stress test of the UK financial market for climate risks this year, following a similar exercise by the Dutch Central Bank. Others, including the Banque de France, Monetary Authority of Singapore, and eventually the European Central Bank, are expected to follow suit in the near term. Many authorities, including the European Banking Authority are also debating the merits of introducing a ‘green supporting factor’2 into macroprudential policy (which could involve preferencing green financial instruments and activities via capital requirements, collateral rules, QE, etc.). Conversely, a ‘brown penalizing factor’ for carbon intensive companies and assets is also being discussed by authorities in some jurisdictions.

In addition, we expect governments may use the low oil price as an opportune window to remove and reform fossil fuel subsidies without the risk of a significant public backlash. Under the recent G20 presidency of Argentina, member states reiterated their commitments, in the medium term, to rationalise and phase out inefficient fossil-fuel subsidies that encourage wasteful consumption (and act as a competitive drag on the economics of clean solutions)3. Lower oil prices dampen the increase in consumer costs caused by reducing or eliminating subsidies and therefore make this G20 initiative more likely to succeed in the nearer term.

Improving economics and efficiency in renewables and batteries makes it harder for legacy energy industries to compete. Innovation and economies of scale are driving down costs for renewables and batteries, and increasing efficiency.

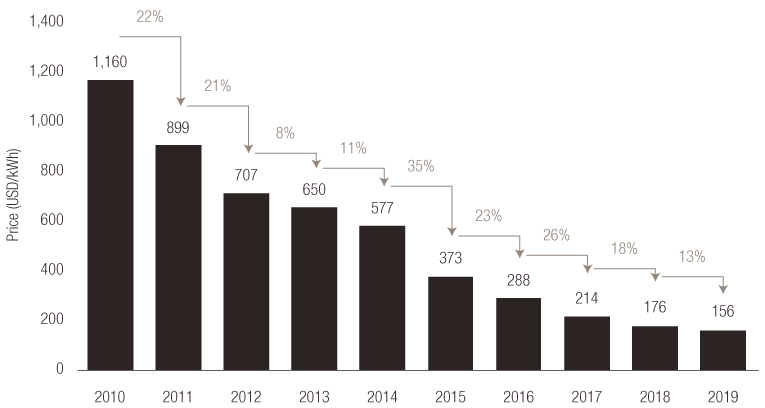

Since 1976 we have seen a rapid fall in the price of crystalline silicon PV modules, down from $80/W to $0.27/W in 2018, and around $0.25/W in 2019. However, just since 2010 PV module prices have fallen by a staggering 85%. Wind technology has also been getting cheaper. The price of wind turbines is down 40% since 2010 on a per megawatt basis. The price of a lithium-ion battery pack is down 87% since 2010 on a volume-weighted basis from $1,160/kWh, to $156/kWh according to BNEF’s December 2019 annual survey. At the same time, battery energy density and cycle life continue to improve – the former up more than 67% since 2011. Like PV and wind, this decline in costs is the result of manufacturing scale and innovation, with battery pack demand rising 100-fold from 2010 to 2018.

Battery cell prices have fallen 87% since 2010

Source: BNEF

Research suggests oil may have to be priced as low as $10-$20 a barrel to remain competitive for mobility purposes4. As renewables and electric vehicles have become more efficient, wind and solar technologies now provide up to seven times more energy for the same cost compared to oil trading at $60 per barrel. Battery production costs are largely immune to oil price dynamics and will continue to decline as economies of scale ramp up and cell chemistry efficiencies accelerate. This will continue to act in favour of EVs and minimise any delay to the cross-over point where EVs cost less to produce than combustion engine vehicles (2025 based on our current projections). From the consumer’s point of view, total cost of ownership (TCO) is reliant more on production costs and vehicle depreciation (a new technology such as electric cars depreciates at a much faster rate in the early years of adoption than a more established technology), than on the spread between petrol and electricity prices.

Natural gas is a ‘frenemy’ of renewables. While it competes in power generation, natural gas prices would have to fall by a very significant margin to offset the advantages of renewables, which are getting cheaper and can be produced at near-zero marginal cost. On the other hand, low oil and gas prices may prove to be supportive of renewables by forcing coal out of the grid. The flexibility of gas supply also means it has a role in stabilising power supply against the high level of variability in renewable power generation before cheap storage is available at scale. This helps smooth the integration of renewables into the energy mix.

There is clearly a short-term risk that the low oil price might postpone private investments decisions on energy efficiency as the implied cost savings might no longer be worth the initial investments. Energy-intensive products might also gain a temporary better competitive positioning near-term. However, we believe these are only temporary factors as stricter regulation is likely to come back into force. This is not the first time the oil price has been through a resetting recently. In 2014, it dropped from on average USD110/bbl to an average USD60/bbl and yet this did not stop the search for energy efficiency in building for instance, as global regulations have tightened.

In the longer term, cheap oil and gas could also be good for the nascent hydrogen economy, although this will depend on many other factors as well. The first major applications of hydrogen are now emerging – in mining, for example. Hydrogen is a central feature of the EU’s Green Deal as the Commission recognizes hydrogen technology “will be strategically important for energy independence and the future of Europe”. Hydrogen also represents an investment opportunity that is better aligned to the engineering expertise and distribution capabilities of oil and gas networks than renewables, where utility companies may have a more natural advantage. Hydrogen, therefore, is a likely candidate of capital moving out of oil and gas industries.

Changing consumer patterns support the transition to net-zero. Consumer awareness of sustainability concerns and demand for more sustainable goods and services is driving a broad, behavioural shift towards more sustainable buying patterns.

The evolution of business models is supporting this change. Across mobility industries, for example, lease purchase is now the predominant model for buying new vehicles in developed markets. This means consumers are increasingly focused on the total cost of ownership (TCO), or monthly auto payments, rather than the upfront vehicle sticker price. This works in favour of EVs, which have a lower TCO than new combustion engines and are even on a par with second-hand combustion vehicles today, when factoring in various local and national incentives. By 2025, we expect a tipping point will occur where carmakers will stop wanting to produce combustion engine cars5 and consumers will see the TCO of EVs fall even further below that of new combustion engine vehicles, even if gasoline prices remain supressed. And with regulation on fleet average emissions enforcing EV adoption, whether consumers want to drive more environmentally or not, we believe a reduced oil price will have little impact on the climate transition already underway in the automotive sector.

COVID-19 will likely dampen any increase in high-carbon consumer demand resulting from lower fuel prices. The International Energy Agency expects oil demand will fall in 2020 for the first time in a decade because of the economic slowdown in China and the disruption to global travel and tourism.

COVID-19 has exposed how elongated our supply chains are and how exposed many value chains are to key components coming from the other side of the world. Re-localisation of production and some form of de-globalisation may occur as a result. In turn, that could deflate global transportation needs from shipping, to trucks and aviation. COVID-19 has also created a demand shock. Renewables can act as a Keynesian solution. An investment-led Green deal could appeal to many governments as a domestic-focused solution for temporarily impaired economies.

Our Climate Transition Strategy focuses on technology solutions and adaptation opportunities that stand to gain market share during such a transition.

Oil suppliers realise peak-oil demand has passed, which will likely extend the price war in the longer-term. Much of the higher-cost oil produced globally in the legacy energy sector is especially problematic for climate change (arctic oil, tar sands, methane flaring from fracking). The risk of producers suffering huge write-downs as a result of ‘stranded assets’ is increasing as momentum builds behind the move to a net-zero economy. The Saudis, who produce some of the cheapest oil globally, may well be seeing the writing on the wall of peak demand. Saudi Arabia is leveraging its oil riches to diversify the economy away from its dependence on fossil fuels, but in the meantime it is using the price war to make sure they win the battle to pump as much oil as possible for as long as possible. If that is the case, low oil prices may be here to stay. This could in turn force capital into more economically attractive opportunities within the energy space and allow much-needed funds to be reallocated from fossil-fuel subsidies to greener investments.

sources.

4 BNP Paribas: Wells, Wires and Wheels… - EROCI and the tough road ahead for oil, August 2019

5 VW will start developing its last mass-market technology for combustion-engine cars in 2026, according to strategy chief Michael Jost. Bloomberg VW Sticks to E-Car Shift as Oil Price Slump Helps Gas Guzzlers, 12/2/2020

important information.

This document has been issued by Lombard Odier Funds (Europe) S.A. a Luxembourg based public limited company (SA), having its registered office at 291, route d’Arlon, 1150 Luxembourg, authorised and regulated by the CSSF as a Management Company within the meaning of EU Directive 2009/65/EC, as amended; and within the meaning of the EU Directive 2011/61/EU on Alternative Investment Fund Managers (AIFMD). The purpose of the Management Company is the creation, promotion, administration, management and the marketing of Luxembourg and foreign UCITS, alternative investment funds ("AIFs") and other regulated funds, collective investment vehicles or other investment vehicles, as well as the offering of portfolio management and investment advisory services.

Lombard Odier Investment Managers (“LOIM”) is a trade name.

This document is provided for information purposes only and does not constitute an offer or a recommendation to purchase or sell any security or service. It is not intended for distribution, publication, or use in any jurisdiction where such distribution, publication, or use would be unlawful. This material does not contain personalized recommendations or advice and is not intended to substitute any professional advice on investment in financial products. Before entering into any transaction, an investor should consider carefully the suitability of a transaction to his/her particular circumstances and, where necessary, obtain independent professional advice in respect of risks, as well as any legal, regulatory, credit, tax, and accounting consequences. This document is the property of LOIM and is addressed to its recipient exclusively for their personal use. It may not be reproduced (in whole or in part), transmitted, modified, or used for any other purpose without the prior written permission of LOIM. This material contains the opinions of LOIM, as at the date of issue.

Neither this document nor any copy thereof may be sent, taken into, or distributed in the United States of America, any of its territories or possessions or areas subject to its jurisdiction, or to or for the benefit of a United States Person. For this purpose, the term "United States Person" shall mean any citizen, national or resident of the United States of America, partnership organized or existing in any state, territory or possession of the United States of America, a corporation organized under the laws of the United States or of any state, territory or possession thereof, or any estate or trust that is subject to United States Federal income tax regardless of the source of its income.

Source of the figures: Unless otherwise stated, figures are prepared by LOIM.

Although certain information has been obtained from public sources believed to be reliable, without independent verification, we cannot guarantee its accuracy or the completeness of all information available from public sources.

Views and opinions expressed are for informational purposes only and do not constitute a recommendation by LOIM to buy, sell or hold any security. Views and opinions are current as of the date of this presentation and may be subject to change. They should not be construed as investment advice.

No part of this material may be (i) copied, photocopied or duplicated in any form, by any means, or (ii) distributed to any person that is not an employee, officer, director, or authorised agent of the recipient, without Lombard Odier Funds (Europe) S.A prior consent. ©2020 Lombard Odier IM. All rights reserved.