global perspectives

Recovery disrupted: as inventories stabilise, wages surge

Welcome to Simply put, where we make macro calls with a multi-asset perspective. This week, we focus on two disruptive forces in the pandemic recovery – inventory shortfalls and rising wages.

Need to know

|

|---|

Disruption: all the rage

‘Disruption’ has been appeared frequently in news reports recently, often accompanied by references to a ‘paradigm shift’. Together, they reflect the pandemic’s deleterious impact on the global production system. The rate of productive capacity utilisation has declined for several months, eroding the productive capacity of the world's major economies. For example, the capacity utilisation rate in the US dropped from 76% to 64% in 2020, but has recently returned to around 75%. Europe experienced a similar decline and rebound, running at 65% capacity at the bottom of the downturn only to return to its pre-crisis level of 80% in the second quarter of 2020. In a world of low inventories, this rapid and prolonged decline in production, followed by a rapid restart, was bound to generate tremors: the so-called ‘disruptions’ we have read about.

In order to avoid the worst enemy of economic analysis – the anecdote – it is essential to classify and then measure such disruptions The press is reporting on surging wages amid severe labour shortages, a lack of raw materials affecting the production of durable goods, and the consequent effects on consumer prices. These disruptions are mainly a reflection of two phenomena: low stock and full order books.

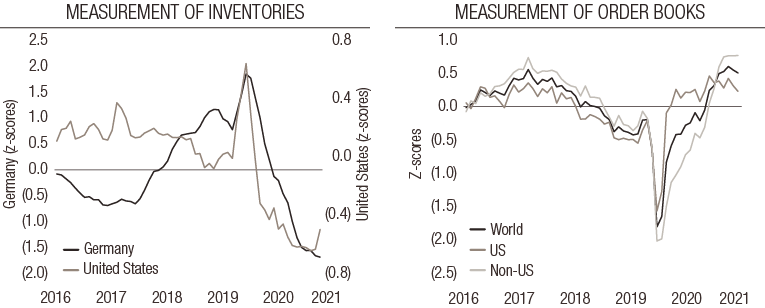

Many business surveys contain questions that accurately measure the state of these two elements around the world. Figure 1 aggregates this data in the form of z-scores: these series are centred and divided by their standard deviation in order to make them comparable and to allow their aggregation. Z-scores mostly oscillate between -2 and +2, with any outliers indicating a score well above/below the long-term average. We use them to provide evidence of ‘disruption’: inventory surveys are abnormally low, while order books are unusually full. This is not isolated to any one country: both the US and Germany exhibit the same trend.

FIG. 1. Measurements of inventories (left) and order books (right) (adjusted to z-scores) for the period 2016-2021

Source: Bloomberg, LOIM as at November 2021.

If we are going to use this scenario to explain how the underlying components of both the consumer and producer price indices are rising, it is essential to look ahead rather than backwards. Both inventories and orders are losing momentum, bringing welcome stabilisation. Of the 36 inventory indicators, 45% are now increasing compared to just 21% in May. Of the 36 order book indicators, only 39% were up in September, compared to 63% in March. If this normalisation continues, prices should gradually adjust.

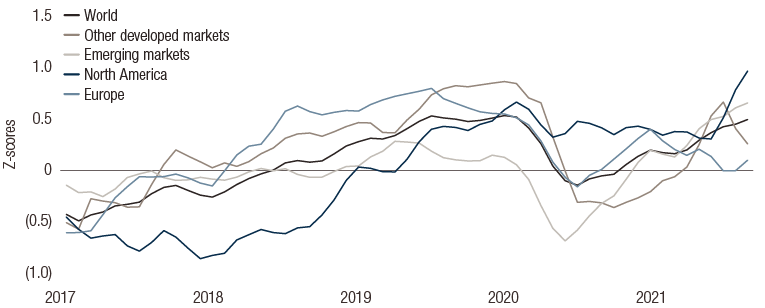

However, another pandemic-related ‘disruption’ does not appear to be weakening: rising labour costs. Figure 2 shows the result of z-score calculations across a wide range of wage-growth measurements1. In 2018-2019, wages generally showed signs of strong growth, but the pandemic brought this to a halt. This year’s recovery drove demand for labour to grow faster than supply. While wages are gradually adjusting, the inertia of wage growth suggests this could be a key feature of the current business cycle. This does not necessarily mean out-of-control wage inflation, but, as central banks have been cautioning for several quarters, inflation could rise above their targets for some time. From a debt perspective, it is essential to keep the spectre of deflation at bay during this stage of the cycle.

FIG. 2. Wage-growth rates (adjusted to z-scores) across the world, 2016-2021

Source : Bloomberg, LOIM as at November 2021.

|

Simply put, the greatest impacts of the pandemic-driven disruptions should now be over and we expect company results to gradually reflect this. However, global wage growth should not be underestimated. Economic theory holds that workers’ pay drives inflation over time, and therefore influences long rates. Investors should closely watch central banks’ reactions to increases in both wages and the cost of capital. |

informations importantes.

À l’usage des investisseurs professionnels uniquement

Le présent document a été publié par Lombard Odier Funds (Europe) S.A., société anonyme (SA) de droit luxembourgeois, ayant son siège social sis 291, route d’Arlon, 1150 Luxembourg, agréée et réglementée par la CSSF en tant que Société de gestion au sens de la directive 2009/65/CE, telle que modifiée, et au sens de la directive 2011/61/UE sur les gestionnaires de fonds d’investissement alternatifs (directive GFIA). La Société de gestion a pour objet la création, la promotion, l’administration, la gestion et la commercialisation d’OPCVM luxembourgeois et étrangers, de fonds d’investissement alternatifs (« FIA ») et d’autres fonds réglementés, d’organismes de placement collectif ou d’autres véhicules d’investissement, ainsi que l’offre de services de gestion de portefeuille et de conseil en investissement.

Lombard Odier Investment Managers (« LOIM ») est un nom commercial.

Ce document est fourni à titre d’information uniquement et ne constitue pas une offre ou une recommandation d’acquérir ou de vendre un titre ou un service quelconque. Il n’est pas destiné à être distribué, publié ou utilisé dans une quelconque juridiction où une telle distribution, publication ou utilisation serait illégale. Ce document ne contient pas de recommandations ou de conseils personnalisés et n’est pas destiné à remplacer un quelconque conseil professionnel sur l’investissement dans des produits financiers. Avant de conclure une transaction, l’investisseur doit examiner avec soin si celle-ci est adaptée à sa situation personnelle et, si besoin, obtenir des conseils professionnels indépendants au sujet des risques, ainsi que des conséquences juridiques, réglementaires, financières, fiscales ou comptables. Ce document est la propriété de LOIM et est adressé à son destinataire pour son usage personnel exclusivement. Il ne peut être reproduit (en totalité ou en partie), transmis, modifié ou utilisé dans un autre but sans l’accord écrit préalable de LOIM. Ce document contient les opinions de LOIM, à la date de publication.

Ni ce document ni aucune copie de ce dernier ne peuvent être envoyés, emmenés ou distribués aux États-Unis, dans l’un de leurs territoires, possessions ou zones soumises à leur juridiction, ni à une personne américaine ou dans l’intérêt d’une telle personne. À cet effet, l’expression « Personne américaine » désigne tout citoyen, ressortissant ou résident des États-Unis d’Amérique, toute association organisée ou existant dans tout État, territoire ou possession des États-Unis d’Amérique, toute société organisée en vertu des lois des États-Unis ou d’un État, d’un territoire ou d’une possession des États-Unis, ou toute succession ou trust soumis dont le revenu est imposable aux États-Unis, qu’en soit l’origine.

Source des chiffres : sauf mention contraire, les chiffres sont fournis par LOIM.

Bien que certaines informations aient été obtenues auprès de sources publiques réputées fiables, sans vérification indépendante, nous ne pouvons garantir leur exactitude ni l’exhaustivité de toutes les informations disponibles auprès de sources publiques.

Les avis et opinions sont exprimés à titre indicatif uniquement et ne constituent pas une recommandation de LOIM pour l’achat, la vente ou la détention de quelque titre que ce soit. Les avis et opinions sont donnés en date de cette présentation et sont susceptibles de changer. Ils ne devraient pas être interprétés comme des conseils en investissement.

Aucune partie de ce document ne saurait être (i) copiée, photocopiée ou reproduite sous quelque forme et par quelque moyen que ce soit, ou (ii) distribuée à toute personne autre qu’un employé, cadre, administrateur ou agent autorisé du destinataire sans l’accord préalable de Lombard Odier Funds (Europe) S.A. Au Luxembourg, ce document est utilisé à des fins marketing et a été approuvé par Lombard Odier Funds (Europe) S.A., qui est autorisée et réglementée par la CSSF.

© 2021 Lombard Odier IM. Tous droits réservés.