Sentiment

Spreads for lower-rated bonds have tightened, compressing relative to higher-rated ones. However, given the prospect of tapering and the risk of interest-rate volatility rising again in the future, we remain constructive on high-yield credit and it continues to be our preference over investment grade. Investor consensus is somewhat one-sided, ‘hoping’ for continued low volatility and a range-bound spread environment ahead. So far, the spill-over from events in China is limited in terms of the wider market, however, this is something we will be monitoring closely.

Technicals

In general, technicals remain highly supportive, with central bank and government policy continuing to be accommodative. Even for September, which is traditionally a strong month for issuance, supply was strong in both the investment-grade and high-yield markets, yet it was matched by demand. However, many deals have featured little-to-no new issue premium, while some higher rated deals have had very low absolute levels. With this in mind, we prefer to await more interesting opportunities.

Valuations

The market continues to be as tight as ever. Investment-grade credit spreads are below pre-Covid levels with little dispersion, while better index quality is driving high-yield valuations back to where they were before the pandemic. Improving fundamentals are translating into more rising-star candidates, supporting high-yield valuations even further. We are keeping our exposure to high yield for its relatively stronger carry, while standing ready to seize opportunities when they arise.

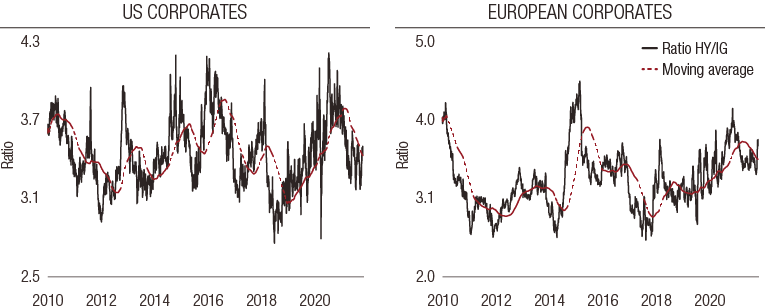

FIG 1. Relative value in corporate bonds: spread ratio of high yield over investment grade

Source: Source: Bloomberg, Barclays as at September 2021. For illustrative purposes only.

Outlook

Q3 results tend to be seen as important indicators of whether businesses will hit yearly performance targets. Overall, the year so far has been quite positive for most sectors, and expectations have increased as a consequence. Most companies are likely to outperform their initial targets from the start of 2021, but equally the market will already expect that. Given the relatively positive environment, companies that fail to meet targets are likely to be punished, although supply issues will inevitably be invoked as an excuse.

With many corporates benefiting from a surplus of liquidity, a key question is what companies will decide to do with all their cash. Will businesses invest in capex, distribute dividends, engage in M&A, or pay down debt?

In our view, the answer to some extent depends on which sector they are in. Some companies may remain cautious at this point, waiting until the end of the year to be sure increased travel and social mixing don’t result in further lockdowns. Others will be keen to repay the expensive debt they issued immediately after Covid hit; we note that firms in challenged sectors such as cruise lines are already carrying out liability management exercises on the debt they issued. Some M&A activity is in evidence, although not all of it successful; for example, the property sector has seen several failed take-over attempts, with insiders seemingly keen to buy but reluctant to sell. M&A could also be favoured in the media sector, where size is becoming key and there is a trend towards concentration, however, valuations are high so deals will not come cheap and companies could become over-leveraged.

In telecoms, the need for continuing investment in the rollout of 5G and fibre means capex will be a key focus, while the historic underperformance of telecoms as a sector pre-Covid means dividends may also be a preferred option. Tech is likely to have a similar focus on dividends and share buybacks. Meanwhile, now that prices have gone up, energy companies are likely to satisfy credit investors by reducing debt, as well as trimming businesses to be more profitable and decreasing the breakeven cost of extracting oil.

To read the full Q4 2021 issue of Alphorum, please use the download button provided.

Sources

1 Any reference to a specific company or security does not constitute a recommendation to buy, sell, hold or directly invest in the company or securities. It should not be assumed that the recommendations made in the future will be profitable or will equal the performance of the securities discussed in this document