investment viewpoints

Climate bonds: investing with impact in the race to net zero

Climate change is a defining challenge of this generation.

Over the next years, investment in climate mitigation and adaptation needs to be scaled up drastically. Investment requirements in the energy system alone are expected to increase to US$ 5 trillion per year by 2030, up from just over US$ 2 trillion today1. Additional investment will be required in infrastructure, nature-based solutions, and the circular economy. But how do investors access these climate opportunities?

Enter climate bonds. A growing and increasingly diverse climate-bond market could help meet the need for this impact capital. One vehicle focused on climate bonds is the Global Climate Bond strategy, launched in March 2017 through a strategic partnership between Lombard Odier Investment Managers (LOIM) and Affirmative Investment Management (AIM).

Global Climate Bond: impact without compromise

The strategy targets mainstream returns and does have an environmental and social impact2. It finances projects in areas like renewable energy, sustainable transport and climate-resilient infrastructure that mitigate or help adapt to the effects of climate change.

The portfolio is aligned to the UN Sustainable Development Goals (SDGs) and the Paris Agreement. Still, we believe it’s important to go beyond alignment and measure and evidence the environmental and social outcomes arising from the investment. This is captured in the Global Climate Bond Impact Report.

The report details how investors have supported efforts to mitigate climate change and promote resilience to its effects. In 2020, the strategy supported 2,330 such projects and initiatives—almost double of the previous year3, largely due to a significant rise in the AUM from last year.

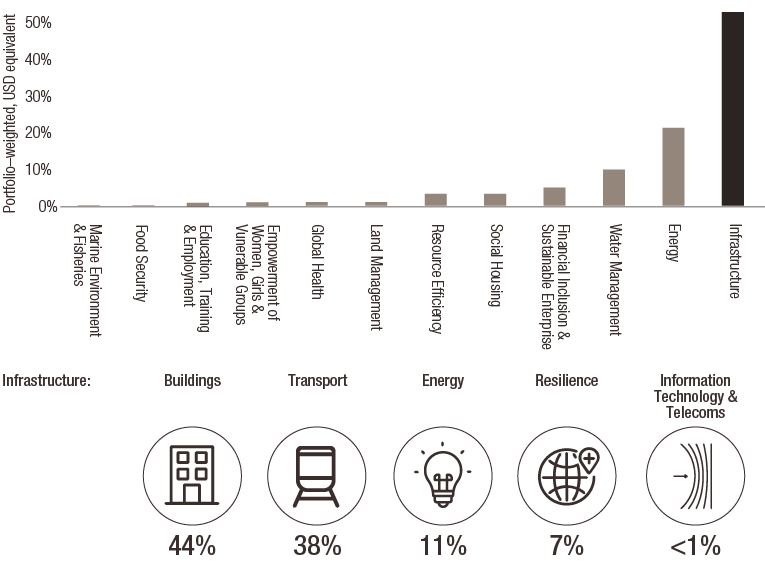

Portfolio allocations

Infrastructure, energy and water were the top three sectors where the impact bond proceeds were allocated. Infrastructure projects included clean transport networks, green buildings, resilience measures and information and communication technology. Buildings were the biggest beneficiary within infrastructure sector constituting a 44% share.

The portfolio also supported 15 of the 17 UN SDGs with the biggest allocation to goals of affordable and clean energy, sustainable cities and communities, and climate action. Mitigation-focused activities constituted 74% of the portfolio whilst 15% was allocated to adaptation-focused projects.

In 2020, the top three sectors that impact bond proceeds were allocated to were environmentally focused.

|

51% Infrastructure |

Hard and soft infrastructure promoting inclusive, climate–resilient, low carbon built environment; for example, clean transport networks, green buildings, resilience measures, information and communication technology. |

Over 7,000 daily passenger capacity supported in low carbon transport. Over 23,000m2 of buildings (by floor area) constructed/refurbished to higher energy efficiency standards |

|

24% Energy |

Renewable energy generation, modern energy access, energy storage and energy efficiency technologies. |

215MW of renewable energy generation capacity supported |

|

|

Water resources management, wastewater treatment, sanitation, water efficiency measures. |

Over 6 million m3 of wastewater treated annually |

Source: AIM Impact report 2020, For Illustrative purposes only

Top portfolio components

Source: AIM Impact report 2020, For Illustrative purposes only

Quality versus quantity

Whilst quantitative measures of impact are important, not all impacts can be verified by numbers. Qualitative observations of impacts achieved complement the hard data and help show how we support several SDGs.

For instance, Burkina Faso, a landlocked country in West Africa, has one of the lowest electrification rates and the most expensive electricity costs within the region. To support the country in scaling up its electrification through solar energy, the FMO Entrepreneurial Development Bank4, a holding in our portfolio, is providing a loan to help finance the development and construction of the Kodeni solar project5.

The solar-power plant is expected to have an annual energy generation capacity of 67.2 GWh. This aligns with SDGs seven and eight – affordable and clean energy and climate action – and could help achieve the government’s target of increasing the nation’s electrification rate to 80%.

Projects like these matter because the rapid scaling up of renewable energy capacity is essential to meet the world’s growing energy demands while reducing overall greenhouse gas emissions. Lack of access to electricity also hurts economic development and impacts people's health and wellbeing – making investments in renewables paramount.

Similarly, power company Vattenfall’s6 Hydrogen Breakthrough Ironmaking Technology project in Sweden is helping fund the production of the world’s first fossil-fuel-free steel by 20267, using green hydrogen and virtually no carbon footprint8. Steel currently accounts for 7% of global carbon emissions and a successful rollout of the project could result in cutting Sweden’s carbon emissions by 10%9.

Other key highlights of the impact report include:

- 126,600 tons of greenhouse gas emissions avoided per year, equating to 70% emissions savings10, compared to a baseline derived from the IEA’s Stated Policies scenario, and calculated using the Carbon Yield® methodology co-developed by AIM

- A coverage ratio of over 90%

- Over 2,330 projects supported in over 160 countries, equating to three quarters of the globe

- Weighted Average Carbon Intensity (WACI)11,12 of about 64 tCO2e/ US$m revenue versus 225 tCO2 e/US$m revenue for the benchmark Barclays Global Aggregate Bond Index, implying a 71% reduction in carbon intensity versus the benchmark

The full report can be downloaded from the Global Climate Bond strategy page.

sources

5 FMO (2021), Sustainability Bonds Newsletter

6 Any reference to a specific company or security does not constitute a recommendation to buy, sell, hold or directly invest in the company or securities. It should not be assumed that the recommendations made in the future will be profitable or will equal the performance of the securities discussed in this document

7 SSAB, Timeline for HYBRIT and fossil-free steel

8 Vattenfall (2021), Green bond investor report March 2021

9 Vattenfall (2021), Green bond investor report March 2021

11 The WACI should be regarded as an assessment of the carbon profile for the share of the portfolio covered by the analysis. The WACI was calculated by maintaining original portfolio weights. The same approach was used for the benchmark.

12 Conducting an issuer-level GHG analysis on fixed income portfolios is a detailed exercise that does not currently benefit from the methodological standardisation and data availability that the equity space has. Moreover, the mapping of sub/supra-national securities and the selection of the most appropriate GHG emission intensity indicator for sovereign bonds are still matters for debate. We have adopted a conservative approach, accepting this may lead to overestimation of the carbon intensity of our portfolios. For example, given the lack of harmonised datasets for sub-national entities, we mapped sub-sovereign issuers to their respective country; for countries’ GHG emissions, territorial emissions were used, even though that might cause double-counting across asset classes. A simplified example of the potential double-counting is a portfolio comprising bonds issued by a corporate domiciled and operating in a country whose government bonds are also held in the same portfolio. The corporate issuer’s emissions arising from domestic sites would also be counted as part of the territorial emissions associated with government bonds issued by the country where the domestic sites are located. These approaches were necessary because of the lack of well-established alternatives.

important information.

For professional investor use only

This document has been issued by Lombard Odier Funds (Europe) S.A. a Luxembourg based public limited company (SA), having its registered office at 291, route d’Arlon, 1150 Luxembourg, authorised and regulated by the CSSF as a Management Company within the meaning of EU Directive 2009/65/EC, as amended; and within the meaning of the EU Directive 2011/61/EU on Alternative Investment Fund Managers (AIFMD). The purpose of the Management Company is the creation, promotion, administration, management and the marketing of Luxembourg and foreign UCITS, alternative investment funds ("AIFs") and other regulated funds, collective investment vehicles or other investment vehicles, as well as the offering of portfolio management and investment advisory services.

Lombard Odier Investment Managers (“LOIM”) is a trade name.

This document is provided for information purposes only and does not constitute an offer or a recommendation to purchase or sell any security or service. It is not intended for distribution, publication, or use in any jurisdiction where such distribution, publication, or use would be unlawful. This material does not contain personalized recommendations or advice and is not intended to substitute any professional advice on investment in financial products. Before entering into any transaction, an investor should consider carefully the suitability of a transaction to his/her particular circumstances and, where necessary, obtain independent professional advice in respect of risks, as well as any legal, regulatory, credit, tax, and accounting consequences. This document is the property of LOIM and is addressed to its recipient exclusively for their personal use. It may not be reproduced (in whole or in part), transmitted, modified, or used for any other purpose without the prior written permission of LOIM. This material contains the opinions of LOIM, as at the date of issue.

Neither this document nor any copy thereof may be sent, taken into, or distributed in the United States of America, any of its territories or possessions or areas subject to its jurisdiction, or to or for the benefit of a United States Person. For this purpose, the term "United States Person" shall mean any citizen, national or resident of the United States of America, partnership organized or existing in any state, territory or possession of the United States of America, a corporation organized under the laws of the United States or of any state, territory or possession thereof, or any estate or trust that is subject to United States Federal income tax regardless of the source of its income.

Source of the figures: Unless otherwise stated, figures are prepared by LOIM.

Although certain information has been obtained from public sources believed to be reliable, without independent verification, we cannot guarantee its accuracy or the completeness of all information available from public sources.

Views and opinions expressed are for informational purposes only and do not constitute a recommendation by LOIM to buy, sell or hold any security. Views and opinions are current as of the date of this presentation and may be subject to change. They should not be construed as investment advice.

No part of this material may be (i) copied, photocopied or duplicated in any form, by any means, or (ii) distributed to any person that is not an employee, officer, director, or authorised agent of the recipient, without Lombard Odier Funds (Europe) S.A prior consent. In Luxembourg, this material is a marketing material and has been approved by Lombard Odier Funds (Europe) S.A. which is authorized and regulated by the CSSF.

©2021 Lombard Odier IM. All rights reserved.