investment viewpoints

Shifting EM correlations create opportunities

Over the past decade, developments in currencies have changed the once strong correlations between all Emerging Market (EM) economies. This expansion warrants focus from investors, as now, we believe, this area of the world offers an increasingly diverse investment opportunity.

EM asset classes, equity and debt, have traditionally been tightly correlated. This stemmed from the fact that those EM assets are expressed in US dollars and thus highly connected to the exchange rate. The correlation was so strong that some deemed it the ‘mother’ of all asset classes and all correlations in these developing countries, with these exchange rate effects magnifying market movements.

As such, when things go well, EM markets rally and EM currencies appreciate against the dollar, benefitting investments. This was the case in 2017. In contrast, 2018 illustrates under-performance due to a double hit taken from both EM currencies depreciating and the underlying assets (both equity and debt) falling too.

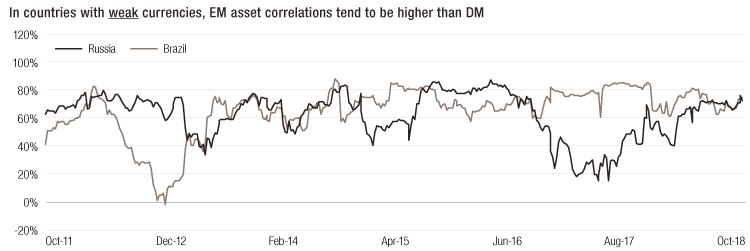

More recently, we see some loosening of this correlation which, we believe, is an early indication of increased diversification and diverging trends within EM. At the country level, there is now more differentiation within each asset class between countries such as Korea and Brazil, or Russia and China. In addition, some EM currencies have grown much stronger than others, creating diverging relative volatility and performance paths for the assets they back.

However, we believe that undertaking such analysis at an aggregated level is too much of a ‘bird’s-eye-view’. Investors should not limit their scope to just country correlations, but also look at correlations between asset classes within each individual country.

Such detailed analysis yields an interesting outcome. Assets of countries with a structurally strong currency show low correlation levels very similar to developed markets’ assets. On the opposite, countries with a structurally weak currency have very strong correlation between their asset classes. As investors, certain measures must be in place to recognise this, as these trends offer risks alongside opportunity.

Emerging market investors typically tend to shy away in volatile times, but we believe that these falling correlations can create an aversion to this. It is therefore apparent, in our view, that an increasingly structured approach to EM assets is required. Firstly, allocations between asset classes need to be on a country-by-country basis. Secondly, currency risk should be mitigated with allocations and hedging for certain countries. Such methodology enables investors to benefit from increased decorrelation and to deliver better risk-adjusted returns with lower volatility.

Analysis conducted by using constituents in JPM GBI-EM for each countries compared with each country’s equity index (in USD)

important information.

This document is issued by Lombard Odier Asset Management (Europe) Limited, authorised and regulated by the Financial Conduct Authority (the “FCA”), and entered on the FCA register with registration number 515393

Lombard Odier Investment Managers (“LOIM”) is a trade name.

This document is provided for informational purposes only and does not constitute an offer or a recommendation to purchase or sell any security or service. It is not intended for distribution, publication, or use in any jurisdiction where such distribution, publication, or use would be unlawful. This document does not contain personalized recommendations or advice and is not intended to substitute any professional advice on investment in financial products. Before entering into any transaction, an investor should consider carefully the suitability of a transaction to his/her particular circumstances and, where necessary, obtain independent professional advice in respect of risks, as well as any legal, regulatory, credit, tax, and accounting consequences. This document is the property of LOIM and is addressed to its recipients exclusively for their personal use. It may not be reproduced (in whole or in part), transmitted, modified, or used for any other purpose without the prior written permission of LOIM. The contents of this document are intended for persons who are sophisticated investment professionals and who are either authorised or regulated to operate in the financial markets or persons who have been vetted by LOIM as having the expertise, experience and knowledge of the investment matters set out in this document and in respect of whom LOIM has received an assurance that they are capable of making their own investment decisions and understanding the risks involved in making investments of the type included in this document or other persons that LOIM has expressly confirmed as being appropriate recipients of this document. If you are not a person falling within the above categories you are kindly asked to either return this document to LOIM or to destroy it and are expressly warned that you must not rely upon its contents or have regard to any of the matters set out in this document in relation to investment matters and must not transmit this document to any other person. This document contains the opinions of LOIM, as at the date of issue. The information and analysis contained herein are based on sources believed to be reliable. However, LOIM does not guarantee the timeliness, accuracy, or completeness of the information contained in this document, nor does it accept any liability for any loss or damage resulting from its use. All information and opinions as well as the prices indicated may change without notice. Neither this document nor any copy thereof may be sent, taken into, or distributed in the United States of America, any of its territories or possessions or areas subject to its jurisdiction, or to or for the benefit of a United States Person. For this purpose, the term "United States Person" shall mean any citizen, national or resident of the United States of America, partnership organized or existing in any state, territory or possession of the United States of America, a corporation organized under the laws of the United States or of any state, territory or possession thereof, or any estate or trust that is subject to United States Federal income tax regardless of the source of its income.

Source of the figures: Unless otherwise stated, figures are prepared by LOIM.

Although certain information has been obtained from public sources believed to be reliable, without independent verification, we cannot guarantee its accuracy or the completeness of all information available from public sources.

Views and opinions expressed are for informational purposes only and do not constitute a recommendation by LOIM to buy, sell or hold any security. Views and opinions are current as of the date of this presentation and may be subject to change. They should not be construed as investment advice.

No part of this material may be (i) copied, photocopied or duplicated in any form, by any means, or (ii) distributed to any person that is not an employee, officer, director, or authorised agent of the recipient, without Lombard Odier Asset Management (Europe) Limited prior consent. In the United Kingdom, this material is a financial promotion and has been approved by Lombard Odier Asset Management (Europe) Limited which is authorised and regulated by the Financial Conduct Authority.

©2019 Lombard Odier IM. All rights reserved